Is Financial Literacy Really the Answer?

An exploration of the factors contributing to the racial wealth divide for African Americans.

By Alexandra Banks

With black wealth being one tenth of white wealth in the U.S., the causes and remedies of the racial wealth gap are a heavily debated topic amongst the black community and economists. Some place the blame on a lack of financial awareness amongst black citizens, attributing a portion of the wealth gap to a lack of financial illiteracy. Similarly, organizations such as the Society for Financial Education and Professional Development have focused their efforts on the overall promotion of financial literacy which frequently targets the youth. Celebrities such as actor Will Smith and rapper Nas have also shown interest in the issue, investing in a financial literacy app for teens.

Often the debate pivots to the efficacy of financial literacy and its use as a tool to combat the shortfall. And with any debate, not everyone agrees with the solution.

“The racial wealth gap is because of historical things that have happened within the country not because blacks don’t have financial literacy…increasing financial literacy is not going to be a remedy for closing the racial wealth gap,” said Dr. Omari Swinton, president of the National Economic Association, a think tank of economists of color promoting economic growth, and chair of Howard University’s economic department.

To understand the current state of the racial wealth gap, the economic history of blacks in America has to be explored.

Since the first enslaved Africans were brought to America, blacks have been at an economic disadvantage compared to whites. While white plantation owners and the common white Americans were building wealth through land ownership, paid labor and the production of cotton and tobacco, blacks were considered property and subhuman.

According to the Economic History Association, “by the mid 1830s, cotton shipments accounted for more than half the value of all exports from the United States.” And “in the seven states where most of the cotton was grown, almost one-half the population were slaves, and they accounted for 31 percent of white people’s income; for all 11 Confederate States, slaves represented 38 percent of the population and contributed 23 percent of whites’ income.”

“When I think of black Americans, I think of people who were brought here to really build wealth for other people and based on that legacy we’re behind,” said Howard University associate professor of finance, Dr. Lynne Kelly.

The gap didn’t stop at the end of enslavement.

Post slavery, the introduction of Jim crow laws in 1877 legalized the enforcement of racial segregation in almost all aspects of public life. Segregation in housing and financial institutions, which are pertinent factors in building wealth, led to institutionalized discrimination and racism towards blacks.

“There have been instances when we haven’t been able to buy homes in certain communities because of things like red lining or banks wouldn’t lend to people of color,” said Dr. Kelly.

The term red lining comes from the practice in real estate where agents would literally draw a red line around a neighborhood on a map, typically poorer communities or communities of color, that they would consider to be a high financial risk which often led to the refusal of service.

“Also, banks historically have not lent money in the same way to our community vs others to do things like start businesses,” she continued.

Prior to the Fair Housing Act of 1968, which prohibits discrimination in “renting or buying a home, getting a mortgage, seeking housing assistance, or engaging in other housing-related activities” there was no protection for blacks and people of color against discrimination from institutions by means of mortgage lending and borrowing, renting and buying homes, and many other housing related services. And although federally outlawed, discriminatory practices in lending still occur today.

“At the peak of the subprime boom African American’s making a quarter of a million dollars a year were more likely to get subprime loans than whites making $35,000 a year on average… for financial literacy to be a driver there you would have to assume that African Americans making $250,000 a year have lower levels of financial literacy than whites making $35,000 and that just doesn’t make any sense to me at all,” said Dr. Jacob Faber, an assistant professor of public service at New York University Wagner.

Through his research in sub-prime mortgage lending, Dr. Faber believes that the discrepancies in racial wealth are due to predatory and discriminatory practices within institutions and should not be considered as a result of financial illiteracy within the black community.

As a result of discrimination within the housing market, Americans are currently experiencing racial disparities in home ownership.

“I think it’s very unlikely to close the racial wealth divide without dealing with the home ownership divide,” said Dedrick Asante-Muhammad, Chief of Race, Wealth and Community at the National Community Reinvestment Coalition, a grass roots organization that aims to help its members build wealth.

“71 percent of whites are homeowners, 21 percent of blacks are homeowners…one huge problem of blacks is that everything they do they get less of a return. So even when we’re homeowners we get less of a return than whites on homeownership,” said Muhammad.

A study on racial disparities in home appreciation from the Center for American Progress, suggests that despite the passing of the Fair Housing Act, there is still residential segregation within homeownership as well as homes within black communities and those of color being worth less than homes in white communities.

The study states that in response to the Great Depression, the government instituted programs such as the Homeowners’ Loan Corporation (HOLC), the Federal Housing Administration (FHA), and the secondary mortgage market which were geared to benefit whites more than blacks through discriminatory borrowing and redlining which has contributed to the current state of the market. The findings include racial steering, a practice of driving homeowners towards or away from certain neighborhoods due to their race.

“There’s a historical perspective from slavery, a racism perspective, and then there’s a literacy perspective…to close the gap we have to do well in those three areas” Kelly continues. Dr. Kelly believes that although financial literacy is not the defining component in closing the racial wealth gap, increasing literacy within the black community would help to reduce the gap.

Conversely, economist and political commentator, Dr. Julianne Malveaux believes the answer to reducing the racial wealth gap can be found in public policy and not in the increasing of black financial literacy.

“That is not a solution to the wealth gap issue. Reparations is a solution to the wealth gap issue,” she said.

She is calling for a change in public policy and a fundamental difference in economics. This she says will be the answer to reducing the current wealth gap.

“Even when poor people are financially savvy, the poverty is structural and has to do with the nature of predatory capitalism in our country,” she said.

The term predatory capitalism refers to the practice of having a select group of people profit at the expense of the rest of those within the economy.

Dr. Malveaux believes that regardless of the financial literacy of marginalized groups within the U.S., the racial wealth gap will persist until institutionalized changes are made.

Like Dr. Malveaux, others argue that the issue is not within financial literacy but the lack of means that would allow one to be financially literate.

“Well you gotta have the income to even work with anything and that’s been the primary issue… We’re the last to be hired, if we are hired. We’re often underemployed,” said Dr. Debby Lindsey-Taliefero, research associate for the Center of Race and Wealth and Howard University professor of economics.

Dr. Taliefero referenced her personal experience with discrimination as it relates to her mother who despite having a collegiate education was only able to obtain work cleaning houses until the NAACP helped her obtain a career within teaching. She feels that despite having the qualifications, African Americans and minorities have historically and continue to be at a disadvantage institutionally which leads to an income disparity.

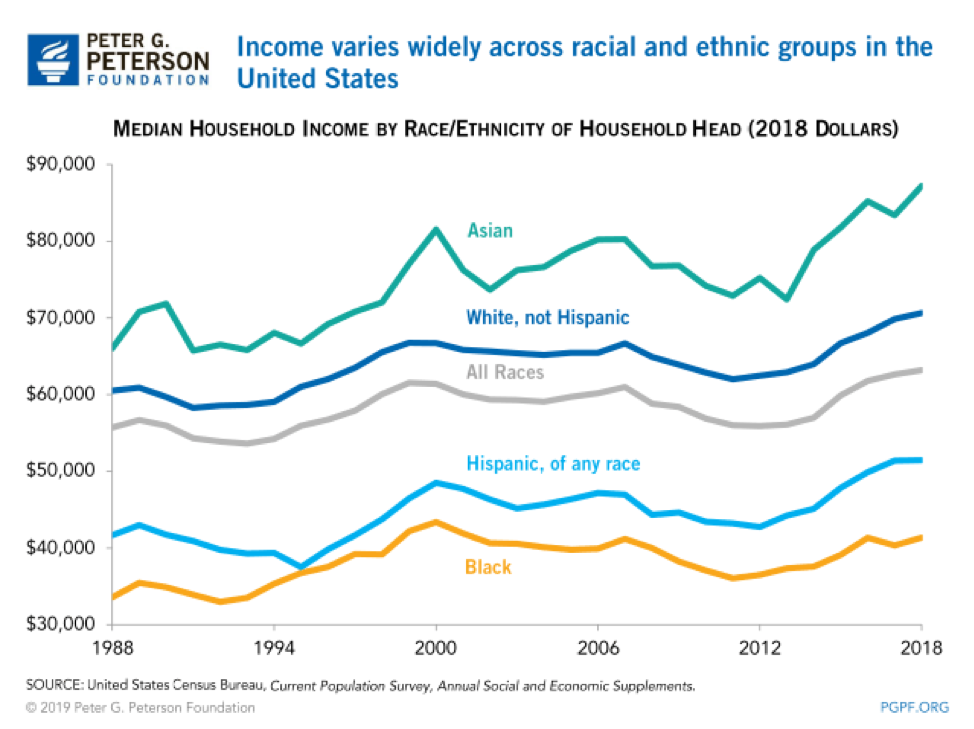

According the 2018 U.S. Census data, black Americans have the highest percentage of poverty at 20.8 percent with Hispanics coming in second at 17.6 percent. As well as Blacks having the lowest median income in 2018 of only $41,361.

Additionally, while financial literacy is an issue, it is not specific to that of the African American community.

In the 2018 Financial Capability study of over 20,000 American adults, only 34 percent were able to answer three or more of the five financial literacy questions asked. Americans overall lack a sense of financial literacy and proper skills to make beneficial financial decisions, it does not appear to be a prominent factor in the outcome of the racial wealth gap.