By Tiasia Saunders

Retirement is what the majority of Americans look forward to after spending decades in the workforce. It comes with financial independence and newfound freedom.

However, Black women are not as supported as their white counterparts in retirement.

Retirement plans are not as popular amongst Black employees, According to Karen Andres, Director of Impact Strategy and Partnerships and Project Director of the Retirement Savings Initiative at the Aspen Institute.

“Black Americans are less likely to have access to a payroll deduction retirement plan at work. According to AARP, only 47 percent of Black employees and 36 percent of Hispanic employees work for a firm that offers a retirement plan, while 58 percent of white workers are offered such a plan,” said Andres.

Those who are offered a retirement plan still face additional obstacles.

“A growing body of evidence, including from our Collaborative for Equitable Retirement Savings, shows that Black women are more likely to take preretirement withdrawals from their retirement account,” she continued.

Historically, Black Americans have had a higher rate of unemployment compared to white Americans. Employed Black Americans tend to work low-earning jobs that don’t offer retirement savings plans.

“I haven’t worked in over 30 years, so no, I don’t have a retirement plan,” said Marylou Chaney, a 63-year-old Black grandmother in Danville, Virginia. “Right now, I use my SSI payments to put a little to the side for my savings account.”

In addition to the lack of retirement plans, single Black mothers struggle to sustain their lifestyles and cannot afford to put away money for future savings.

This could lead to a generational cycle of poor financial decision-making and a lack of information about the importance of a retirement plan.

“When you don’t have a second parent in the house to help with finances and childcare, then you’re at a significant disadvantage, ” said Chris Woods, founder of Silvis Financial, a financial planner service.

“As a result, you’re not able to save nearly as much. You’re not able to think about retirement savings when you’re more concerned with covering present expenses,” Woods continued.

According to the Urban Institute, factors such as state policies, discrimination, segregation, and health disparities contribute to Black women’s overall low wealth. Additionally, some Black Americans lack trust in financial markets due to structural racism.

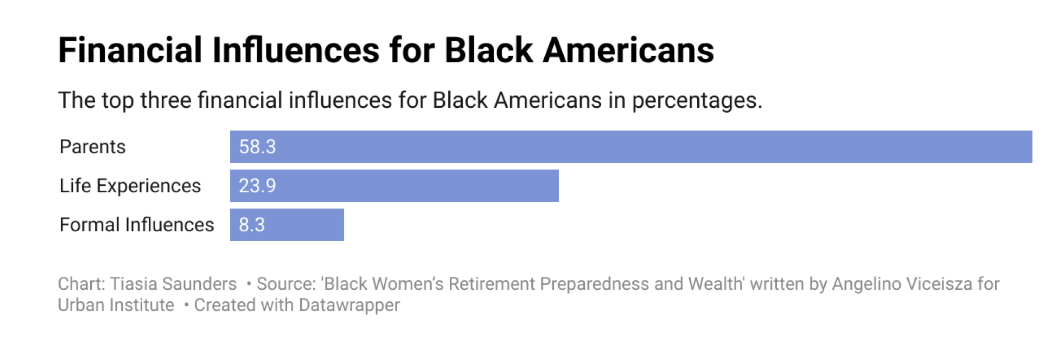

Chart represents the various influences and obstacles that prevent Black Americans to obtain wealth in America. (Tiasia Saunders, HU News Service)

“From a policy perspective, we need to ensure that all workers in America – including Black women – have access to workplace retirement savings, ideally with automatic enrollment. We also need to experiment with ways to help Black women access liquidity in case of an emergency so that they don’t have to withdraw money before retirement,” Andres said.

The Urban Institute’s Office of Race and Equity Research offers a plan to help adjust to how finance is thought about amongst Black Americans and how the workforce compensates Black women..

“One key for every person, particularly Black women, is to try to defer enough in their 401k to get the full match available from their employer,” Woods said. “If you can’t afford to contribute that much, then start with something and try to add 1% a year. If you get a raise, don’t spend more. Add the amount of your raise to savings,” she said.